Executive Interview: Frank Schlehuber, aftermarket director, CLEPA, on automotive remanufacturing in Europe

13-Apr-2022

The remanufacturing industry has existed for several decades, but while operations began as small businesses, the past few years have seen participation from OEMs and tier-1 suppliers, which have begun to see its economic and environmental benefits. Remanufacturing makes an important contribution to achieving the carbon dioxide (CO2) reduction targets that the European Commission is striving for with the Green Deal, and its role has been recognized in the European Commission’s Circular Economy Action Plan as well.

The Brussels-based European Association of Automotive Suppliers (CLEPA), which represents over 120 of the world's most prominent suppliers of car parts, systems, and modules, has taken several measures to promote automotive remanufacturing. They include launching its REMAN Policy Working Group to raise awareness and develop a favorable legislative framework for the industry.

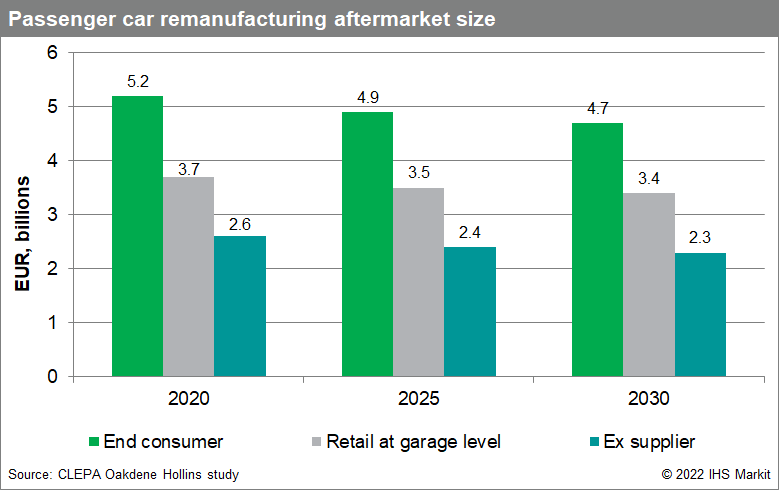

CLEPA, together with consultancy Oakdene Hollins, published a study in November 2021, which estimated that remanufacturing saved more than 800 kilotons of CO2 in 2020, an amount equal to the annual carbon emissions of 120,000 EU citizens. A total of EUR4.7 billion’s worth of remanufactured spare parts were sold by suppliers during the year.

With the transition to more electric powertrains and more electronic content in vehicles, CLEPA believes remanufacturing will be key to avoid shortages in raw materials, and it will offer cost-efficient solutions to consumers over the lifespan of a vehicle.

The transition to electric vehicles (EVs) will result in a complete overhaul of the remanufacturing industry in the long term. The potential market for remanufacturing of EV components is projected to grow significantly, albeit from a low base, touching EUR120 million in 2030, according to the CLEPA and Oakdene Hollins study. The study added that for a smooth transition to an EV portfolio, investment and R&D into EV component remanufacturing will be necessary from today.

This study values the 2020 passenger car remanufacturing market at EUR2.6 billion (ex. supplier level) and estimated it to slightly decline to EUR2.3 billion in 2030, driven by the decline of diesel powertrains, with the impact of electrification expected to be felt after 2030.

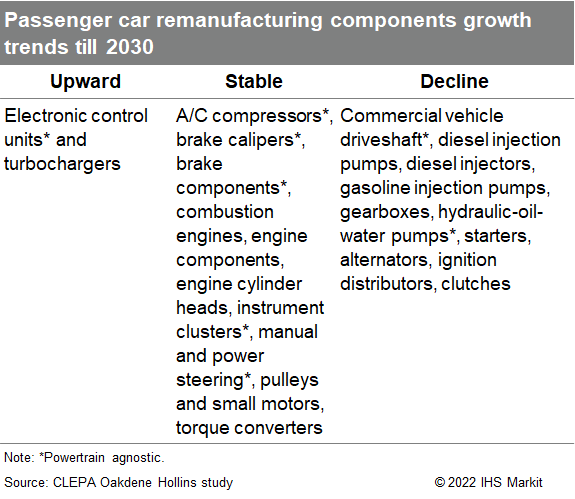

Powertrain agnostic components, such as A/C compressors, brake calipers, combustion engines, and brake components, are expected to remain relatively stable over the next decade, while diesel components are anticipated to decline.

In contrast, the market for commercial vehicle component remanufacturing, at an ex. supplier level, is estimated at EUR2.1 billion in 2020 and is expected to remain stable to 2030. Commercial vehicle components, such as power steering and pumps, electronic units, air brake components, and calipers, should remain stable; diesel injection pumps, EGR, diesel particulate filters, and turbochargers will likely decline.

Please read the edited excerpts from the interview with Frank Schlehuber below:

How would you describe the current state of the automotive remanufacturing industry in Europe and its contribution to the region’s circular economy?

Remanufacturing is key for a circular economy in the automotive sector. Evaluating its contribution in reducing the CO2 footprint requires going into detail and therefore we have analyzed every component subject to remanufacturing. These are broadly engine and drivetrain-related components, but also include steering, calipers, starters, and alternators.

However, we found that in the last few years, a trend called “new-man” (short for new manufacturing) has emerged. These parts are reverse-engineered parts meeting the price points of remanufactured parts but do not have the same specifications. Wholesale distributers have also shown a preference to sell such parts, in order to avoid expenses for the reverse logistics (from the workshop back to the wholesaler and to the remanufacturer often via a collection center) and the management of deposit-payments-binding liquidity. Therefore, “reman” or remanufacturing faced an increasing competition in the past years from new parts with lower specification especially when it comes to starters, alternators, and calipers.

Nevertheless, remanufacturing is an established industry with participation of major suppliers, primarily tier-1s, and some independent remanufacturing specialists. The good thing is, the market will not change overnight: there will be another decade in which the traditional remanufacturing business remains stable, probably even gets boosted. With increasing supply chain constraints, raising raw material prices, and limited availability of semiconductors, remanufacturing might be the solution to ensure parts availability over the lifespan of vehicles.

Other drivers for remanufacturing are corporate sustainability considerations within the automotive sector and the Green Deal targets of the European Commission with circular economy as one main pillar. Remanufacturing has the potential to save greenhouse gas [GHG] emissions in the entire value chain.

As adoption of electrification gains pace, what are the potential new opportunities for remanufacturers?

I share your concern that EVs have a dramatically lower amount of components (than internal combustion engine [ICE] vehicles). This will result in less components for remanufacturing, and parts such as engine parts, starters, and alternators for instance, are no longer needed for battery-electric vehicles [BEVs].

On the other side, electrified vehicles, such as hybrids, provide even more potential for remanufacturing, since additional to the traditional powertrain, starter generators or e-motors are also subject to remanufacturing. With the trend to electric drives, the demand doesn't disappear immediately—it just shifts over to other components. Sure, long-term cylinder heads and cylinder blocks might not be needed anymore, but there are still globally 1.4 billion light vehicles and a vast number of trucks in the world, so their need will not go away immediately.

EVs will have new components, such as electric motors, inverters, or complete e-axles, and such motors have a substantial share of copper, which is a high-value, precious metal. Copper parts were always subject to remanufacturing, and I cannot imagine that they will be replaced by new components in case of defects. EV components also contain other metals of high value. EV components have the potential to be remanufactured, and I clearly see companies already investing in this space. I'm not talking battery cells—that is a separate emerging business—but even without the battery, there are enough components in EVs that are subject to remanufacturing. Due to cost, availability, and sustainability reasons, suppliers will be challenged by OEMs to come up with repair or remanufacturing solutions early in the development stage. I think that the remanufacturing landscape will reshape substantially in the next three to five years.

From a legislative point of view, what are the key drivers for remanufacturing?

We have legislation in Sweden and in France, which promotes the use of reused parts and the mandatory offer to consumers as an alternative option to new parts. The mandatory use of remanufactured components if technically possible is one potential driver, but I expect more pressure from the sustainability discussion. For the aftermarket, we as suppliers are in discussions with wholesaler organizations to define principles for a sustainable aftermarket. Suppliers have laid out principles, and these include the recommendation to not only offer remanufactured parts but also the relevant information to allow the remanufacturing of parts. So, the sustainability discussion will definitely drive that remanufacturing mindset.

What do you consider as the main challenge for the remanufacturing industry?

One of the problems is that more and more parts depend on software. The gearbox, for example, might come with basic software from a supplier, but gets a specific data set from an OEM. Without a vehicle-specific data set, it cannot be operated. This means [that] it's getting increasingly complex to transfer components from one car to another, but remanufacturing involves doing exactly that. Increasing cybersecurity measures or IP-protected software will give OEMs more control over and better access to the remanufacturing business.

Another challenge is that some companies have stepped away from remanufacturing due to the availability of cheap new components and the resistance from wholesalers to carry remanufactured components, including management of deposits and reverse logistics.

Besides that, another challenge for remanufacturing is the accounting standards, which in Europe are not clear about how to treat cores, as waste or raw material with a value which can be estimated only after disassembly and inspection.

What are the possible solutions to address the issue of accounting standards and core liability?

I think we should consider a common standard on how to value and treat cores and related materials under accounting principles, because it's not waste. Therefore, this [is] an aspect where I see a need to step in and work with companies facing these issues.

Remanufacturing depends on a core return system, and this needs to be as lean as possible. Currently, the biggest issue is the deposit payment for the cores. The deposit is collected and kept until the part is returned. In practice, the deposit is collected mostly because there is no trust among business partners. A remanufacturer who does not get defect parts back is missing raw material and is forced to purchase cores. There are brokers offering workshops more money than they’ve paid to collect cores, and the cores are then sold to remanufacturing facilities at a premium. Artificial bottlenecks such as these result in increasing what is a bit of a challenge for the remanufacturing industry. Therefore, it is critical to have a unique, error-proof system for core management that is agreed upon by all stakeholders. Presently, human intervention is high, but if there is a legal ground and a software solution to support this, it will be the way to go.

What policy interventions can boost remanufacturing uptake in the short-to-medium term?

We are trying to get a legislation that helps the industry and the environment. One aspect of our efforts is the Motor Vehicle Block Exemption Regulation (MVBER). But the latest indication from the European Commission is that there will be no change in the regulation, just an extension until 2028. This means that we rely only on the Vehicle Repair and Maintenance (RMI) legislation, which is embedded in the Type-Approval Regulation. Here, OEMs must ensure that independent operators have easy, restriction-free, and standardized access to information on the repair and maintenance of vehicles, but often, Intellectual Property Rights (IPR) or Design or Tooling Rights or unreasonable fees or not granted licenses erect barriers for independent aftermarket.

So, what’s the solution? Of course, legislative measures, but that’s the long way to go. The technical aspect of remanufacturing will be more complex and more restricted and therefore, finding a technology partner or collaboration models here will be the key. Meanwhile, I think the market will reshape and new collaboration models among market actors will emerge. None of the current market players cover everything that is needed to be competitive in the future technical environment: OEMs might have the competence and access to relevant software but are missing the creativity of a remanufacturing specialist and the deep product knowledge of a suppliers. And this is the reason why I say this market (remanufacturing) will reshape completely in the upcoming years.

Nishant Parekh, Senior Research Analyst, Automotive Supply Chain, Technology and Aftermarket, IHS Markit (now part of S&P Global)

nishant.parekh@ihsmarkit.com