While 2025 reinforced that the fundamentals were supportive, it also clarified that in 2026, aftermarket players who can manage complexity around diagnostics, calibration and data access will be able to capture more value.

The automotive aftermarket continues to remain structurally supported by the growth in the vehicle parc and vehicle age, even as stricter tariff measures have disrupted global supply chains and heightened uncertainty.

There are expected to be about 371 million out-of-warranty vehicles in Europe by the end of 2026, accounting for roughly 84% of the region’s total vehicle population. This means the aftermarket will have a vast pool of vehicles to support with parts, servicing and repairs.

By the end of 2026, over 132 million vehicles on European roads will have some form of advanced driver assistance systems, and over 26 million will have Level 2 and above autonomy capabilities. By 2035, over 111 million vehicles in Europe will have Level 2 and above features. This widespread integration of ADAS into vehicles will require aftermarket suppliers and workshops to adapt their service capabilities and business models to meet the demands of these complex systems.

Our report, Top Aftermarket Trends 2026, builds on the success of 2025’s publication. It explores the impact of global macroeconomic trends, studies vehicle-in-operation (VIO) trends, evaluates the rapid expansion of ADAS in today’s fleet (which is reshaping aftermarket industry dynamics) and examines the most recent changes in the global right-to-repair movement.

Automotive aftermarket industry trends: Key highlights

An expanding fleet continues to offer support

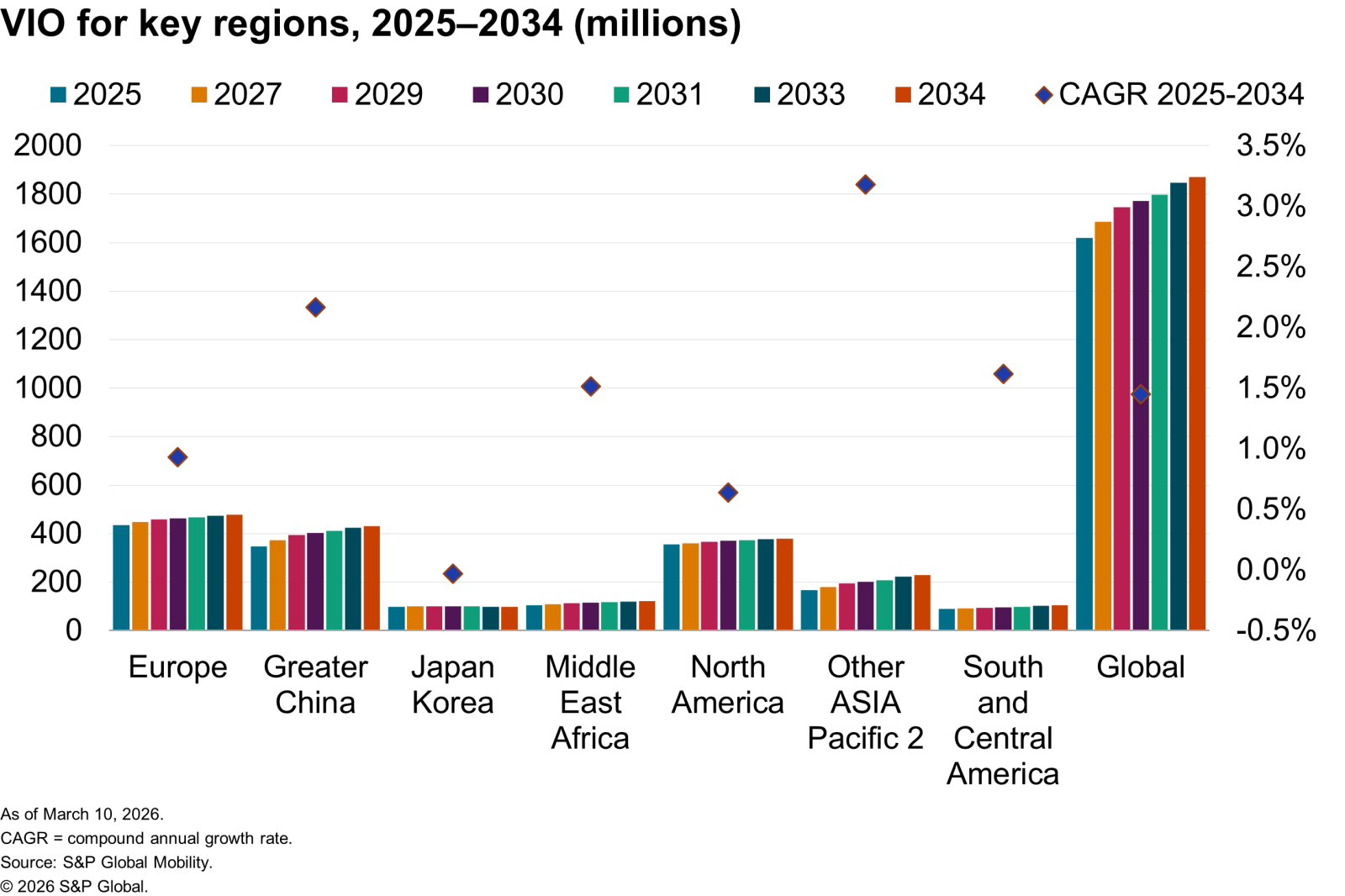

The global number of VIO is forecast to continue growing, reaching 1.9 billion light vehicles by 2034, compared with 1.6 billion in 2025. VIO growth is driven by Other Asia and Greater China regions, which have an annualized return of 3.2% and 2.2%, respectively, between 2025 and 2034.

Europe is the largest VIO market globally and has the highest average number of light vehicles. It is expected to cross 14 years in 2026, rising to 16 years by 2034. Rising new vehicle prices, uncertainty around battery-electric vehicles (BEVs) and the reliability of older vehicles, along with affordable maintenance, are key factors in driving up the age.

India continues to have the fastest-growing VIO among major markets, while growth in Japan and South Korea is expected to stagnate. Europe will see the share of BEVs in its VIO growing at a pace only second to Greater China by 2034.

Aftermarket distributors resilient to major shocks, but face tariff and economic pressure

Our financial analysis of major automotive aftermarket parts distributors in the previous five years revealed that they recorded the lowest revenue growth rebounds compared to original equipment manufacturers and suppliers after the pandemic. Lower but continued usage of vehicles and demand for replacement parts limited the impact.

Between 2020 and 2023, while the revenue growth of aftermarket distributors was slower compared to OEMs and suppliers, they showed resilience in their net income margins by outperforming the other two groups. Post 2023, economic challenges have impacted all stakeholders. In the past five years, companies such as Autozone Inc., O'Reilly Automotive and Genuine Parts Co. recorded strong profitability and capital efficiency compared to other distributors, according to our analysis.

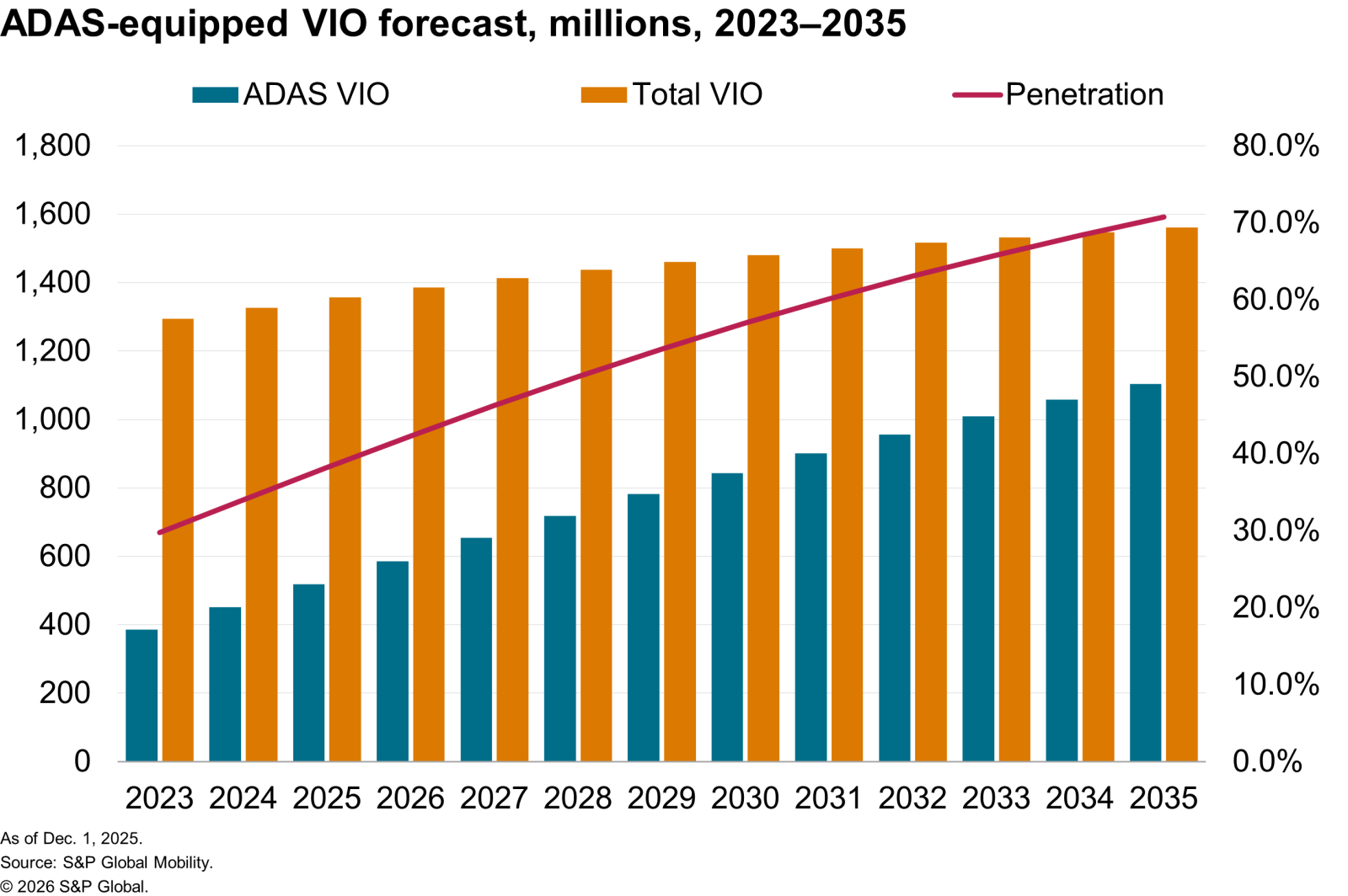

Growing ADAS vehicles in the fleet offer opportunities for the aftermarket

The rising adoption of ADAS is driving higher penetration rates within the VIO and creating maintenance and repair opportunities in the aftermarket, including calibration and replacement services.

By 2035, over 1.1 billion VIO globally are expected to feature various levels of ADAS, at a CAGR of 8.5% from 2024. Adoption is projected to reach 71% of VIO in 2035, compared with 38% in 2025. By 2035, over 82% of the vehicle parc in Greater China, 69% in North America and 62% in Europe will be equipped with ADAS, up significantly from 2025 levels.

Our analysis shows that Level 2/Level 2+ autonomy will grow rapidly, thanks to technological maturity, economies of scale and regulatory pressures, amid Level 3’s limited market potential.

Meanwhile, autonomous vehicles have advanced swiftly from testing to the initial stages of commercial deployment. Here, Greater China is at the forefront as well, thanks to proactive government policies, simplified regulations and extensive access to real-world driving data for robo-taxis. Level 4 VIO in Greater China is expected to be nearly three times that of North America by 2035.

Tariffs could weigh on aftermarket revenue, but sector better suited than others to manage uncertainty

The automotive aftermarket, already contending with a challenging consumer environment, is now grappling with evolving tariffs and trade policies. The tariff measures have introduced new challenges, affecting global supply chains, sourcing strategies, cost structures and more.

Tariff disruptions could cut 5-6% of aftermarket revenue, cause delays and erode suppliers’ bottom line, according to the US Auto Care Association’s 2026 Auto Care Factbook. In 2023, the US imported US$139 billion in aftermarket auto parts, with 47% sourced from Mexico, 12% from Canada, 8% from Mainland China and 33% from the rest of the world. The tariffs imposed in mid-2025 were expected to add US$22.4 billion in duties.

While the automotive aftermarket is better positioned than most retail subsectors to weather higher tariffs, players across the supply chain will need to diversify to maintain business continuity amid shocks. The US automotive aftermarket is expected to grow by 5.1% in 2025 to US$434.9 billion, after 5.7% growth in 2024, before recovering in 2026.

Clarity around right-to-repair crucial to independent aftermarket growth

The consumer right-to-repair movement and the topic of access to repair data continue to see heightened discussion from automotive trade bodies globally.

In the US, although the REPAIR Act has not yet been enacted, a US House Subcommittee held a hearing to explore it in January 2026. Automaker trade bodies say that as vehicles become increasingly complex and software-driven, access to repair and diagnostic data will be critical to ensuring safe, affordable repairs.

In Europe, the movement is centred on the Motor Vehicle Block Exemption Regulation (MVBER). In April 2023, the European Commission prolonged the regulation until May 31, 2028. Aftermarket players believe the rules now face growing constraints. There is a need for an updated framework after 2028 to align with the aftermarket’s digital transformation.

On Mar. 19, 2026, CLEPA, the European Association of Automotive Suppliers said that access to in-vehicle data needs further guidance under the European Commission’s Data Act. Its Secretary General Benjamin Krieger stated that delays in implementing frameworks that enable open and fair data markets risk substantial losses for companies and could weaken Europe’s competitiveness. The association has urged policymakers to expand the Commission’s guidelines for the Data Act “to better address competitive dependencies”.

In Australia, right-to-repair reform, implemented in July 2022, has led to a 6.7% increase in industry turnover, equating to A$2.4 billion in growth, according to the Australian Automotive Aftermarket Association. Additionally, there has been a 40% reduction in instances where repairers had to turn away vehicles due to inaccessible repair information.

Author: Nishant Parekh, Senior Research Analyst, Automotive Supply Chain, Technology and Aftermarket (nishant.parekh@spglobal.com)